What Insurance Do Gig Workers Need? A Complete Guide for Independent Contractors

See How We're Different

or call us: (858) 384‑1506

What Insurance Do Gig Workers Need to Protect Themselves?

Roughly 38% of Americans are gig workers, and this number is continuing to rise. Unlike traditional employees, gig workers are responsible for their own insurance. The type of insurance varies by the nature of the work, but most gig workers face real risks, and those who work through an app may face gaps in coverage.

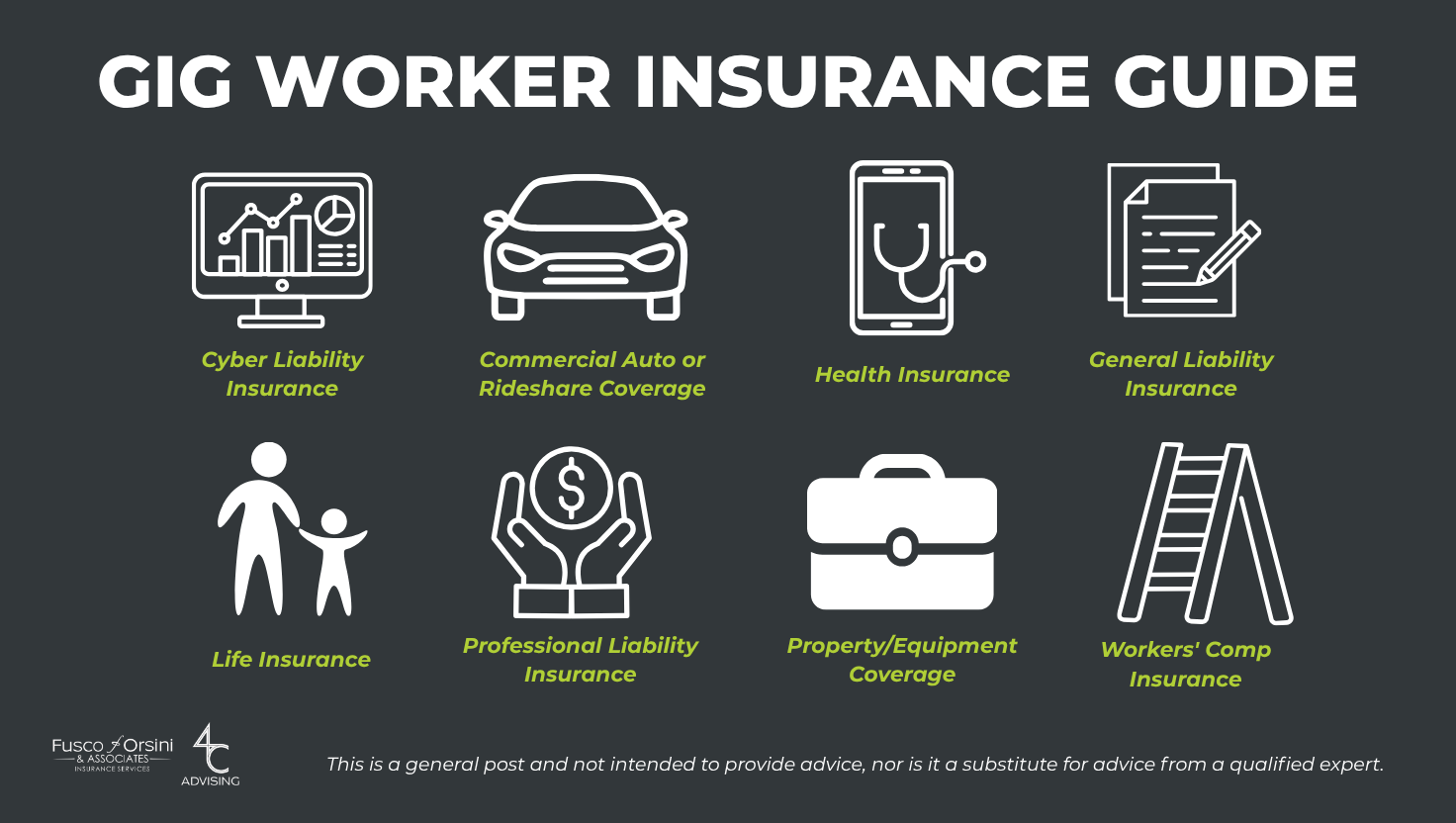

Most gig workers should consider general liability, professional liability, commercial auto insurance, health insurance, and income protection (such as disability).

Understanding the coverage you need and gaps you face will help protect you, others, and your future. We break this down below.

What is a Gig Worker?

A gig worker is a person who does project-based, temporary, or on-demand jobs. They are paid by the “gig” instead of earning a salary through traditional, full-time employment.

Common examples of gig workers include rideshare and delivery drivers, freelancers (like designers, writers, and consultants), pet sitters, home service providers, photographers, virtual assistants, tutors, and other independent contractors hired for specific projects.

Because gig workers are not employees, they are usually classified as independent contractors. As such, they are not eligible for employee benefits and need to manage their own taxes, schedules, and insurance.

Gig Worker vs. Independent Contractor: What’s the Difference?

Gig workers are independent contractors, which is why the terms are often used interchangeably. However, being a “gig worker” is not how you are classified; it simply defines the type of work arrangement you pursue.

People are often attracted to gig work because it offers the opportunity to control their time, schedule, and how much they work. Gig work also provides an income opportunity for those surviving layoffs, and/or needing to pick up additional income.

The challenge gig workers face is that they are less protected, which is why it’s especially important to talk to an experienced insurance professional who can advise on the best insurance coverage options.

Common Gig Worker Insurance Myths

- Myth: gig workers are fully covered by the app they work through, like Uber.

- Myth: personal auto insurance covers incidents involving gig work.

- Myth: a gig worker is “too small” or can fly under the radar.

- Gig workers may underestimate their coverage needs or overestimate current coverage.

- Myth: gig workers don’t need workers' comp since they don’t employ anyone.

What Insurance Do Gig Workers Need? (Key Coverage Types Explained)

Now that we’ve dispelled common myths around gig work and insurance, let’s dive into reality.

There are five main insurance categories gig workers should consider:

Commercial Auto or Rideshare Coverage: This can provide liability and vehicle damage coverage when using a personal car on the job. Personal auto insurance typically excludes gig-related driving.

Example: Your personal auto policy denies a delivery accident claim.

Cyber Liability Insurance: Anyone handling client data online should strongly consider purchasing cyber liability insurance. Additionally, adopting cybersecurity best practices is essential (see 9 Common Cybersecurity Mistakes Remote Workers Make). Remember, a lot of business is conducted online, even for non-tech companies!

Example: Client data is compromised through your email, and you're liable.

General Liability: This insurance covers claims arising from third-party injuries, property damage, or personal and advertising injuries. It may also cover associated legal defense costs.

Example: A client trips over your equipment and gets injured.

Health Insurance: Coverage through the ACA Marketplace or Medicare can help with doctor's visits, prescriptions, lab work, and hospital care.

Example: A single hospital visit generates a bill you wouldn’t be able to pay out of pocket.

Life Insurance: This type of insurance provides financial support for beneficiaries if the gig worker passes away.

Example: If you were to pass away, life insurance could help your family cover costs like your mortgage, rent, or bills.

Professional Liability Insurance: (also known as errors and omissions insurance) protects against claims of negligence or mistakes, specifically addressing financial losses clients may face related to your services.

Example: A mistake costs a client thousands, and you must pay.

Property/Equipment Coverage: Insures tools and equipment against theft or damage, such as a stolen camera or specialized tools.

Example: Your specialized tools are stolen during a job.

Workers' Comp Insurance: This one may be surprising, but it’s worth considering, especially for those working in environments with a higher risk of injury. It’s worth noting that in California, app-based gig workers are usually classified as independent contractors, meaning they are not protected by the app company’s workers' comp policy. Disability insurance is another option gig workers may consider if they can’t work due to injury or illness.

Example: You injure your back on the job and can't work for weeks.

When Does App Insurance Cover Gig Workers, and When Does It Not?

For independent contractors working through apps like DoorDash, Uber, or TaskRabbit, there’s a lot of confusion about when coverage begins and ends. The short answer is that it usually depends on what phase of work you’re in.

“It's important for the gig worker to know where the app/platform liability coverage ends and when theirs begins,” says Chris Jorge, broker at Fusco, Orsini & Associates Insurance Services. “Gig workers should connect with an insurance professional to review all insurance documents closely and to get a clear understanding of their responsibilities and liability.”

How Much Does Gig Worker Insurance Cost?

Premiums vary based on many factors, such as the nature of your work, how much you work, where you work, claims history, policy limits, and more.

Next Steps

If you are a gig worker, it’s time to think about insurance not as a backup plan, but as an active way to protect yourself, others, and your tools and equipment. You’ve already taken the courageous step of “going solo”, but you don’t have to be solo in your insurance journey. We’re here to help! Get started HERE.

Sources:

Zywave: Infographic: Do Gig Workers Need Insurance?

AI Disclosure:

Portions of this content were generated with the assistance of ChatGPT (OpenAI) on March 25, 2026, and reviewed by our insurance team for accuracy.

Disclaimer:

This information is intended for reference only and should not be considered as financial or legal advice. Consult with a qualified professional for personalized guidance.

Recent Post