What Are My Benefit Limits for 2026 and How Do They Compare to 2025?

See How We're Different

or call us: (858) 384‑1506

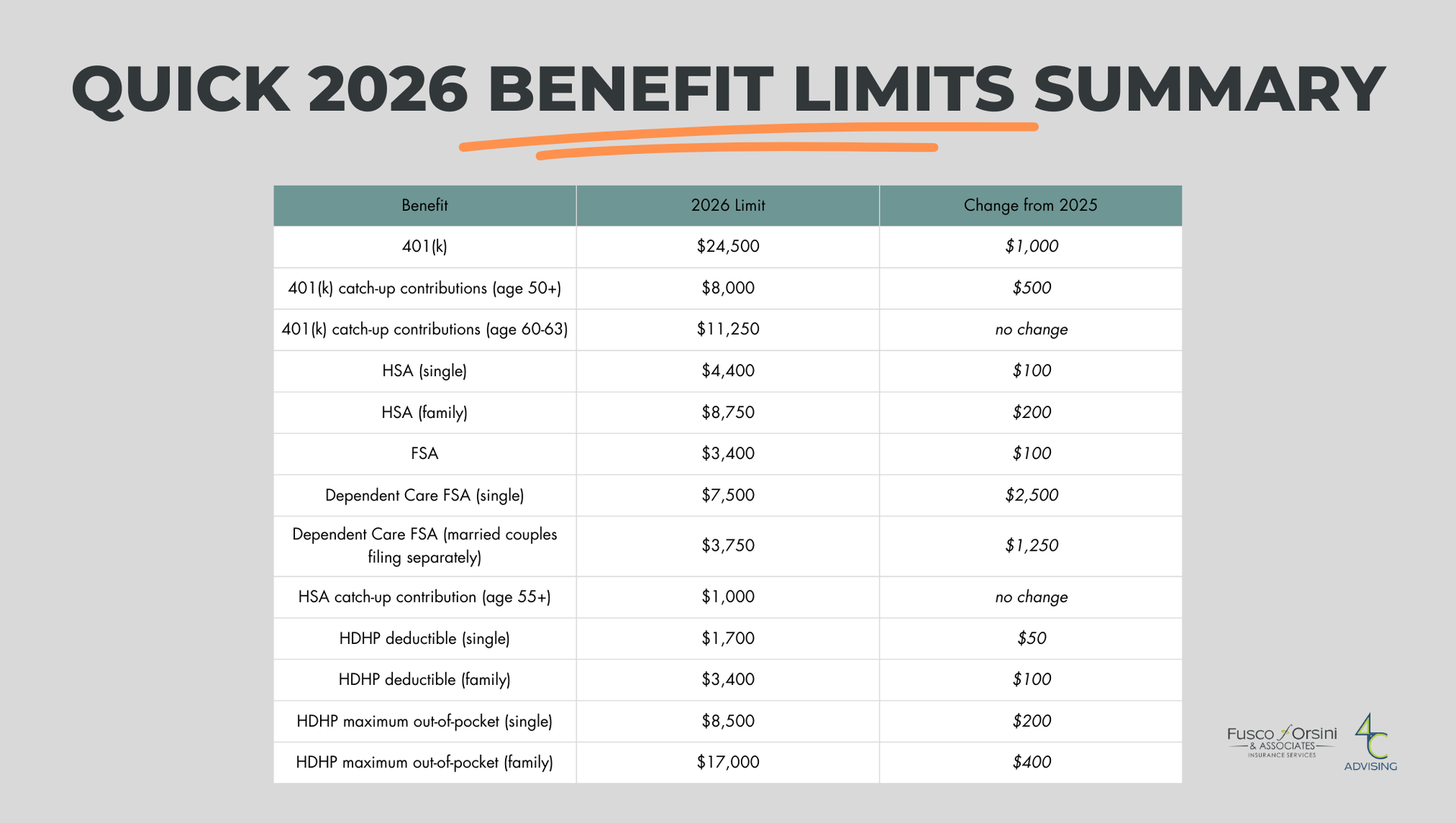

Quick Summary: In 2026, contribution limits increased for 401(k)s, HSAs, FSAs, and HDHP out-of-pocket maximums. These changes can impact your tax savings, healthcare costs, and retirement planning.

If you’re asking, “What are my benefit limits for 2026, and how do they compare to last year?” you’re not the only one. Benefit limits change, and understanding these changes can help you and your team make smarter decisions during open enrollment and throughout the year.

Below, we break down the 2026 limits for the most common employee benefits, including 401(k)s, HSAs, HDHPs, and FSAs, and we highlight what has changed from 2025.

401(k)

What is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to contribute a portion of their paychecks, either pre-tax or Roth, toward retirement, often with employer-matching contributions. Funds can grow tax-advantaged until withdrawal in retirement.

What are the 401(k) contribution limits for 2026?

- Employee contributions:

$24,500

up $1,000 from 2025 - Catch-up contributions (age 50+):

$8,000

up $500 from 2025 - Catch-up contributions (ages 60 to 63):

$11,250

no change from 2025

These limits apply per person, across all 401(k) plans you participate in.

What are the advantages of a 401(k) in 2026?

- Contributions are automatically deducted from your paycheck, making savings automatic.

- The pre-tax contributions reduce taxable income on every paycheck.

- Many employers offer matching contributions, which increase your total retirement savings.

Health Savings Account (HSA)

What is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a tax-advantaged account used to pay for qualified medical expenses if you’re enrolled in an HSA-eligible High Deductible Health Plan (HDHP). Funds roll over year to year and stay in your hands, even if you change jobs.

What’s new for HSAs in 2026?

According to the IRS, the One Big Beautiful Bill (OBBB) has expanded HSA eligibility:

- Telehealth services can be covered before meeting the deductible without affecting HSA eligibility

- Bronze and catastrophic plans offered through an Exchange are now considered HSA-compatible, even if they don’t meet the traditional HDHP definition

What are the HSA contribution limits for 2026?

- Self-only coverage:

$4,400

up $100 from 2025 - Family coverage:

$8,750

up $200 from 2025 - Catch-up contribution (age 55+):

$1,000

(no change from 2025)

Note: Contribution limits include both employee and employer contributions combined.

What are the advantages of an HSA in 2026?

- Contributions are tax-deductible or pre-tax

- Funds roll over and can be invested

- Withdrawals for qualified medical expenses are tax-free

- HSAs can be used as a long-term healthcare and retirement savings tool

High Deductible Health Plan (HDHP)

What is a High Deductible Health Plan (HDHP)?

A High Deductible Health Plan (HDHP) is a health insurance plan with lower monthly premiums and higher upfront costs. You typically pay 100% of most medical expenses until you meet your deductible, after which costs are shared through coinsurance or copays. HDHP enrollment is required to contribute to an HSA.

What are the HDHP limits for 2026?

Minimum deductibles

- Self-only:

$1,700

up $50 from 2025 - Family:

$3,400

up $100 from 2025

Maximum out-of-pocket limits

- Self-only:

$8,500

up $200 from 2025 - Family:

$17,000

up $400 from 2025

What are the advantages of an HDHP?

- Lower monthly premiums

- Eligibility to contribute to an HSA

- Annual out-of-pocket maximum protects against worst-case medical costs

Flexible Spending Account (FSA)

What is a Flexible Spending Account (FSA)?

A Flexible Spending Account (FSA) is an employer-sponsored benefit that allows employees to set aside pre-tax dollars to pay for eligible healthcare expenses such as copays, prescriptions, dental, and vision care.

What’s the difference between an FSA and an HSA?

- FSAs are employer-owned, which means you can’t take the contributed funds with you if you leave

- Most FSAs are use-it-or-lose-it, meaning you have to use and claim funds by the end of the year.

- Alternatively HSAs are employee-owned, roll over year to year, and can be invested.

What are the FSA contribution limits for 2026?

- Healthcare FSA:

$3,400

up $100 from 2025 - Dependent Care FSA:

- $7,500 (single), up $2,500 from 2025

- $3,750 (married couples filing separately),

up $1,250 from 2025

Why this matters:

Understanding benefit limits helps you:

- Maximize tax savings

- Avoid unexpected out-of-pocket costs

- Choose the right plans for your health and financial goals

If you have questions about how these limits apply to

your specific benefits, our Employee Benefits team is here to help.

BOOK TIME WITH AN EXPERT.

Sources:

Zywave, 2026 Limits to Know

Investopedia, Maximize Your HSA: Tax-Free Growth and Retirement Healthcare Savings

AI Disclosure:

Portions of this content, including example benefit-related questions, were generated with the assistance of ChatGPT (OpenAI) on January 12, 2026, and reviewed by our Employee Benefits team for accuracy.

Disclaimer:

This information is intended for reference only and should not be considered as financial or legal advice. Consult with a qualified professional for personalized guidance.

Recent Post